Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- The Boeing 767 Cross Section, Part 1 November 24, 2022

- Movie Review: Devotion November 21, 2022

- China will accelerate development of its commercial aerospace sector November 21, 2022

- Bjorn’s Corner: Sustainable Air Transport. Part 46. eVTOL comparison with helicopter November 18, 2022

- The economics of a 787-9 and A330-900 at eight or nine abreast November 16, 2022

Odds and Ends: Russian MC-21 subsidy; C919 assessment; ExIm countdown

Two news items popped up today on emerging aircraft.

MC-21 subsidy: Government subsidies for commercial aircraft development have been a sore point between the US and Europe (i.e., Boeing and Airbus) for decades. Although the US and Europe went through years of international disputes at the World Trade Organization on behalf of Boeing and Airbus, with adverse decisions now under appeal by both sides, and even though Canada and Brazil previously won cases over illegal subsidies to Embraer and Bombardier, nothing has come of the decisions–and nothing has been done about government subsidies by Japan and China to their aerospace industries. No complaints to the WTO have been filed against either country, which are members of the WTO.

This article updates some information about Russian aid to Irkut, which is developing a competitor to the Airbus A320 and Boeing 737 families. The MC-21 and China’s COMAC C919 are directly sized against the best-selling single-aisle airplanes. Russia is not a member of the WTO, so there is no legal basis (that we know of) to file a complaint.

Long-time readers know we disdain the entire WTO process anyway as more political than practical. The WTO has no enforcement powers and sanctions that might be authorized by the WTO against offenders don’t have to be implemented (as in the case of Canada and Brazil) or even applied against the offender’s products–another industry altogether may be sanctioned, a silly and unfair prospect.

C919 assessment: This article provides an assessment of the prospects for the COMAC C919. What’s especially interesting in this article is what we aviation geeks have known all along, and that is China uses Western technology to develop its airplanes (and trains, the article points out). Airbus and Boeing identify China as the next viable competitor in the airliner field, albeit perhaps a generation in the future. But the technology is coming from Airbus, Boeing, Embraer, Bombardier, the engine makers and the supply chain. They are creating their own future competitors.

While China’s industrial espionage contributes to its understanding and acquisition of Western technology, most of it comes from joint ventures between Chinese companies and the Western OEMs and suppliers.

ExIm countdown: The authorization for the US Export-Import Bank expires next month, and Boeing is pulling out all stops to get a recalcitrant Republican Party to agree to extend the life of the bank, reports The Hill, one of the specialty publications that covers the US Congress.

Killing ExIm will put Boeing at a disadvantage to Airbus, which uses and will continue to use European Credit Agencies (ECAs) to support sales of its aircraft. Boeing will have to fall back on its internal Boeing Capital Corp. or attempt to help customers find private financing if ExIm tanks.

Odds and Ends: GAO report on ‘Boeing’s bank;’ C919; Airbus widebody strategy

GAO report on ‘Boeing’s bank:’ The US Government Accounting Office, a non-partisan investigating agency, completed a study of the funding and guarantees provided by the US ExIm Bank, which is under criticism from Congressional Republicans, and concluded non-US airlines do benefit from what amounts to subsidies.

These put US competitors at a disadvantage, GAO concludes. The full 29 page PDF may be found here.

The study period covered the global financial crisis, during which a good deal of private capital funding dried up. Airbus and Boeing each relied more heavily on export credit agencies for customer financing–ExIm in Boeing’s case and collectively European Credit Agencies, or ECAs, for Airbus.

The GAO found that ExIm funded or guaranteed financing for 789 Boeing wide body aircraft while the ECAs supported 821 Airbus wide-bodies.

Parenthetically, this statistic alone should demonstrate to Congress the need for ExIm to continue to be available for Boeing airplanes.

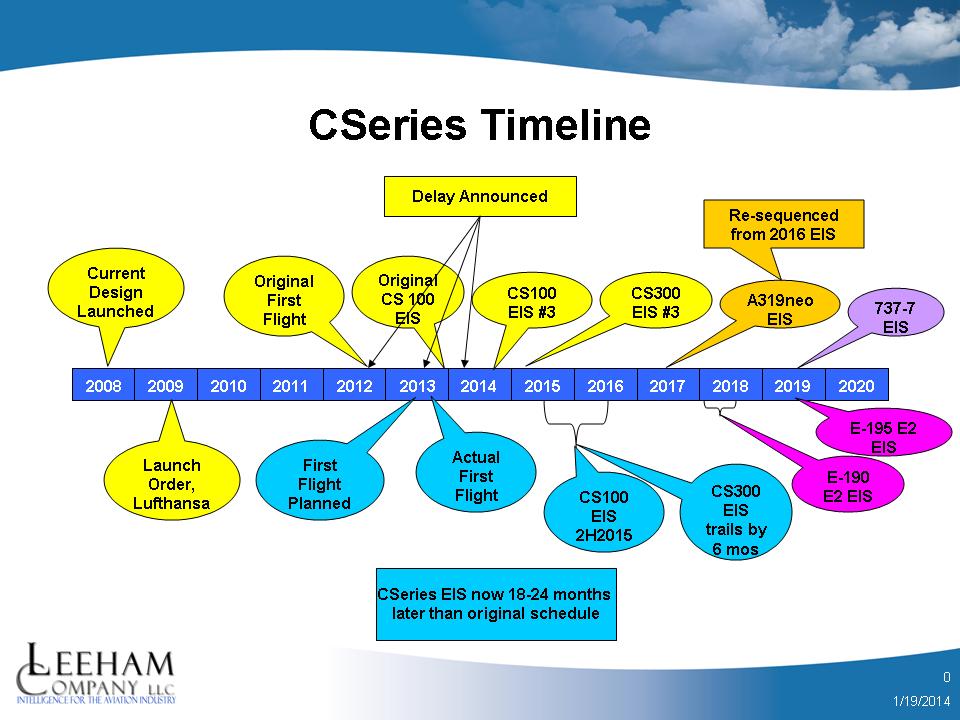

Odds and Ends: CSeries timeline; KC-46A roll-out; China’s new airplane

CSeries timeline: Bombardier last week announced a third delay in the CSeries program, this time for as much as a year.

This probably should have been expected. BBD originally planned a five year period between program launch and entry-into-service. As we saw with the Boeing 787, launched with a four year timeline, even five years was too ambitious.

CSeries Timeline. Leeham Co Chart

The EIS period for the 787 turned out to be the standard seven years, almost eight–and even then, the EIS was anything but smooth.

Airbus’ launch-to-EIS for the final A350 version is somewhat more than eight years. Even though BBD is a sub-contractor on the 787 program and said it benefited from lessons learned, it’s clear officials were far too ambitious.

KC-46A roll-out: Boeing’s first tanker for the USAF based on the 767-200ER will roll out this summer. The Everett Herald has this story. The airplane is a somewhat revised 767-200ER called the 767-2C. In addition to upgrades with the airframe, the Pratt & Whitney PW4000 engines will have upgrades which improve fuel consumption.

China’s new airplane: China isn’t just developing the ARJ21, C919 and some military airplanes. It’s also developing the world’s largest amphibian.

GE analysis post Farnborough

Our wrap up of Farnborough would be incomplete without looking closer at the world’s leading engine supplier, GE Aviation, which together with partners (like SAFRAN in CFM joint venture) garnered more than $36 Billion in orders and commitments during the show. This figure was only significantly bettered by Airbus ($75 Billion) and it came close to Boeing’s $40 Billion. With such level of business the claim by GE Aviation CEO, David Joyce, that the Airbus A330neo engine business was not the right thing for GE as they have more business than then they know what to do with, was certainly no case of “sour grapes”. Read more

68 Comments

Posted on July 28, 2014 by Bjorn Fehrm

Airbus, Airlines, Boeing, Bombardier, CFM, Comac, CSeries, Embraer, Farnborough Air Show, GE Aviation, Leeham News and Comment, Pratt & Whitney, Rolls-Royce, Uncategorized

737 MAX, 777, 777-300ER, 777X, 787, A320NEO, A330neo, Airbus, Boeing, Bombardier, CFM, Embraer, Pratt & Whitney, Rolls-Royce